The FAQs are AI-generated, and Fortune India is not responsible for its content or any associated copyright issues.

I would describe myself as collegial

/ 4 min read

I would describe myself as collegial

This summary is AI-generated, and Fortune India is not responsible for its content or any associated copyright issues.

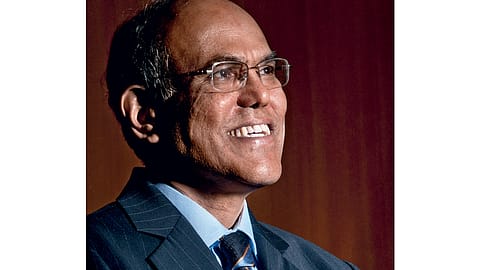

He’s been criticised for destroying business sentiment. RBI governor D. Subbarao explains his hawkish policy stance to T. Surendar. Edited excerpts:

Q: Before the financial crisis, many economists believed that central banks should restrict themselves to targeting inflation and not look at financial stability. India seems to have proved that wrong.

Before the crisis, one of the popular beliefs used to be that if you have price stability, financial stability is an automatic byproduct. But we now know that financial stability has to be treated as an independent variable. Indeed, if price stability continues for too long, you should be concerned about some cancerous underbelly in some parts of the economy. Even orthodox inflation targeters believe that central banks must have some responsibility and obligation towards financial stability.

In India, because of the wide mandate enjoyed by the Reserve Bank, we have always had a fairly large responsibility for financial stability. The world view is coming round to our viewpoint but that doesn’t mean that we don’t need to change. The dimensions of financial stability are getting more complex, and it cannot be handled by RBI alone. The government and other regulators need to be involved too. What their role will be in times of crisis and in peace is something we need to settle between ourselves. And that comes with experience.

Q: As someone who believes in consensus, how do you manage the fine balance between the demands of inflation management and keeping the growth story alive?

More than [a believer in] consensus, I would describe myself as being collegial. Building consensus is difficult, but I do try to consult people from outside, as well as my colleagues in the top management. I am also conscious of the fact that the final call rests with me. However, today’s debate is driven by a misunderstanding of the growth-inflation tradeoff. It is not that you can have high growth if you settle for high inflation. The short-term Phillips Curve theory has been discredited and is certainly not applicable to India. Actually, when we are fighting inflation, we are not fighting the pro-growth people, but trying to reach the same destination through different means. It is my view that when inflation is this high, you first need to bring it down in order to make growth sustainable.

Q:What are the checks and balances you have put in place to ensure that the banking sector is safe when you issue banking licences to the corporate sector?

From the constitution viewpoint, we have said that new banks will be promoted by non-operating holding companies. There is a prescription about the number of independent directors on the boards of such companies; some stipulation about how much capital they need to start with, and how they should dilute it over time.

There are prescriptions about exposure of the bank to the promoter group as well. We have also sought some amendments to the Banking Regulation Act to give RBI the power to approve anyone acquiring 5% or more of shareholding in a bank from the “fit and proper’’ prospective. We have also asked for power to supersede the board of the bank. These are some safeguards we have instituted in the draft guidelines based on marshalling international experience and our study of the Indian situation. More important than what we prescribe is how we enforce these regulations. We need to improve our skills and proficiency for regulation and supervision.

RANK

COMPANY NAME

REVENUE

(INR CR)

(INR CR)

{{#current-rank}} {{current-rank}} {{/current-rank}} {{^current-rank}} {{rank}} {{/current-rank}} {{name}} {{#revenue}} {{revenue}} {{/revenue}} {{^revenue}} {{noi}} {{/revenue}}

Q:There was a perception that you were a finance ministry man when you assumed office. But over time, you seem to have found an independent voice.

I am certainly a finance ministry person more than any other governor because I walked straight into RBI from North Block within 24 hours. But that’s where it ends. The fact that I have been selected for this job means that the government has confidence in me, as in the previous appointees. But as far as autonomy is concerned, it comes partly with the job. Not only in India but around the world, governments are jealous about the autonomy the central banks enjoy and the central banks guard their autonomy quite jealously. That is in the natural order of things and it is not with reference to any particular set of people in any particular position at this point of time.

Q: When you took over, you said you wanted to make the central bank more transparent.

A lot has been achieved, but much more needs to be done. I want the RBI’s accountability as an institution to go up. Accountability is not only about supply accountability but also demand. But that can only happen when people know what RBI does. One of the main planks of demystifying the office of governor is to tell people what it does, why it does, and what the challenges and dilemmas are, so that they can ask the right questions.

The most important component is the outreach programme, where senior executives of RBI and commercial banks, along with district administrators, visit villages and explain to the people what we do. We also try and reach out to the young population through town hall meetings. I am very conscious of the demographic dynamics of the country, where a number of people are below 30 and we must listen to their hopes, aspirations, and demands because they are the future. We have also tried to make the monetary policy communication more systematic and more easily understandable.

Frequently Asked Questions

Explore the world of business like never before with the Fortune India app. From breaking news to in-depth features, experience it all in one place. Download Now